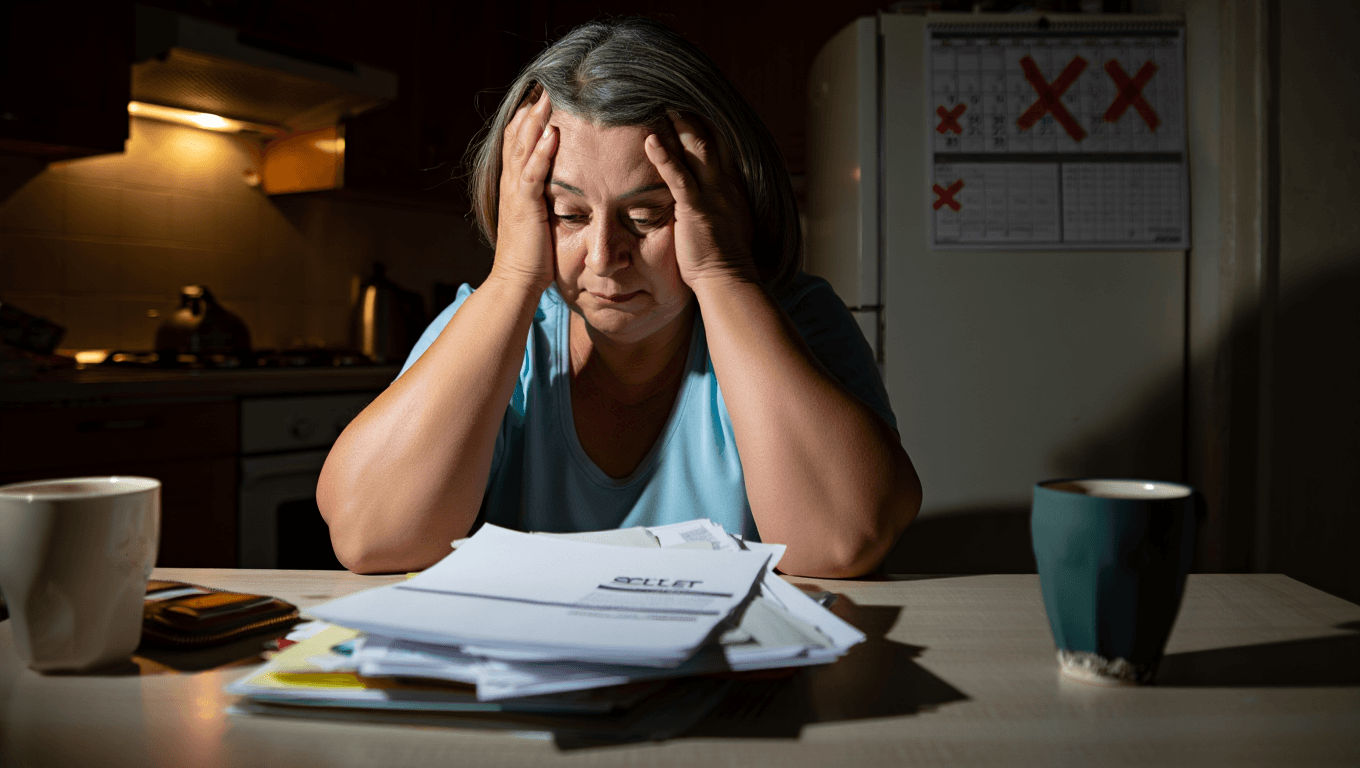

The latest Consumer Financial Resilience Index, released this month by a consortium of economic researchers, signals a subtle but important shift in household stability that could affect spending, borrowing and policy decisions in the months ahead. A decline in savings cushions and rising debt burdens — concentrated among younger and lower-income households — makes the index a timely barometer of how prepared consumers are for new shocks.

Designed to capture more than headline indicators such as unemployment or inflation, the index aggregates several measures of household financial health. It combines data on income volatility, access to credit, debt servicing costs, and emergency savings to produce a single snapshot of how resilient households would be if faced with a loss of income or a sudden expense.

What the index measures and why it matters now

The index’s relevance has grown as interest rates remain elevated and the cost of living continues to be volatile. When resilience erodes, discretionary spending tends to fall quickly; that can ripple through retail, services and the labor market. Lenders and policymakers watch the index as an early warning signal: a weakening score can precede increases in loan defaults or slower consumer-driven growth.

Key components of the index include:

- Savings buffer: the typical household’s emergency funds measured in months of expenses.

- Debt service ratio: the share of income committed to servicing loans and credit obligations.

- Income stability: frequency and magnitude of earnings fluctuations, including gig and contract work.

- Credit access: availability and cost of borrowing, from credit cards to personal loans.

Recent trends and who is most exposed

In the most recent quarter the composite index edged lower after several quarters of plateauing, driven mainly by two forces: slowly rebuilding savings are outpaced by rising borrowing costs, and income volatility has ticked up among younger workers. The decline is not uniform — households with higher incomes and larger liquid assets remain relatively stable, while renters, recent graduates and single-earner families show the largest deterioration.

Regional differences also appear. Areas with higher housing costs are showing weaker resilience, reflecting the interaction between mortgage or rent burdens and limited disposable income. Conversely, regions with stronger wage gains have seen only marginal weakening.

Implications for consumers, lenders and policy

For consumers, a lower resilience score means less capacity to absorb unexpected expenses without resorting to high-cost credit. For banks and other lenders, it increases the likelihood of tighter underwriting and higher interest terms for riskier borrowers. Policymakers face a delicate balance: measures to boost incomes or expand safety nets could shore up resilience, but tighter monetary policy aimed at controlling inflation can further strain debt-laden households.

| Component | Direction this quarter | Why it matters |

|---|---|---|

| Savings buffer | Small decline | Fewer households can cover 3+ months of expenses without borrowing |

| Debt service ratio | Rising | Higher interest costs reduce discretionary income |

| Income stability | More volatile | Gig and irregular work increase downside risk |

What to watch next

Over the coming quarters, trends to monitor include wage growth relative to inflation, consumer credit delinquencies, and whether precautionary savings begin to rebuild. Any significant shock — a sharp energy-price rise, a regional labor disruption, or rapid policy shifts — could amplify the index’s movements.

Analysts say the index offers a forward-looking lens: it doesn’t predict a recession, but it does quantify how large and how immediate the consequences of one might be for households. The practical takeaway for observers and decision-makers is simple — small shifts in resilience can translate quickly into broader economic effects.

As researchers refine the metric and update it with more granular data, the Consumer Financial Resilience Index will continue to be a useful tool for tracking the financial health of households and anticipating where vulnerabilities are growing.

Similar Posts

- Oil surge pushes bond yields higher: investors brace for higher borrowing costs

- Fed signals final rate cut in 2025: Here’s how it could impact your finances

- Credit card debt knocks out dating prospects for 1 in 6 Americans: survey

- Financial literacy check: uncover costly money blind spots today

- Majority of consumers expect rising prices by 2026: New outlook report reveals worrying trends

An expert in international finance, Jessica provides actionable advice to secure export transactions and minimize financial risks.